How to Make a Budget and Stick to It

Action Step 3 - Categorize your spending

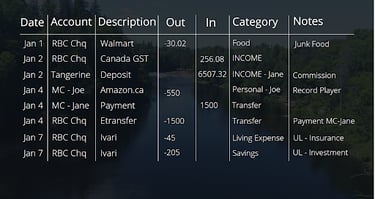

Select range and sort by Description A-Z; this makes it easier to label categories.

Create categories that make sense to you and don't leave any transaction without a category. Refer to your receipts as needed.

Total each category.

To help you get started, feel free to use or modify the categories I use for my budget tracker:

Expenses:

Business (tax deductible expenses for my business),

Entertainment (subscriptions to streaming services, memberships to museums, etc.),

Fees (extra fees like interest paid, late penalty; money that didn’t need to be spent),

Food (junk food, restaurants),

Fuel,

Gift,

Grocery (food, toiletries, essential supplies),

Living Expense (utilities, phone, insurances, fees that cannot be avoided, mortgage, pet expenses, car payments),

Medical (prescriptions, kids’ braces, chiropractor, massage, etc.)

Personal - (Name) (wants, cosmetics, clothes; often what doesn’t fit in other categories),

Misc. - (Name of Store) (if I lose the receipt and don’t remember what I purchased)

Other:

INCOME - (Name),

Transfer (When transferring money between accounts, e.g. credit card payment). Delete every transfer after they’ve all been matched.

Reimbursement (money received or to be received back).

Savings (investments)

Action Step 4 - Review your cash flow

Review what’s going into your accounts and what’s coming out. Take a look at your spending habits and look for opportunities to save money.

How well do you keep receipts so every transaction is properly categorized?

Is there more money leaving your account in certain categories than expected? Why?

Are there charges you don’t recognize?

Are you spending more for something that you can get cheaper somewhere else for equal or better quality?

Do you have a positive cash flow (more money coming in than going out) or do you have a negative cash flow (more money going out than coming in)?

If you had a positive cash flow, are you living the life you want?

Based on your cash flow, how long will it take to achieve each of your financial goals?

Knowing where you are now and having a clear vision of where you want to be are the first major steps to achieving your goals which is why keeping a financial journal (aka. budget tracker) is so important.

Action Step 5 - Stop the bleeding

Stop wasting money in areas that don’t affect your lifestyle, e.g. Some insurance companies charge 3-10x more for the same coverage.

Make healthy lifestyle changes. It may be difficult in the beginning but to limit junk food, quit smoking, reduce alcohol and coffee intake, avoid gambling; these don’t just lead to a healthier you, they lead to a healthier savings account.

Replace high interest debt with low interest (see https://www.101money.ca/highinterestloans)

Action Step 6 - Don’t subtract…add.

Add a financial professional. Just as an excellent doctor can show you how to improve your overall wellbeing, an excellent financial advisor can show you how to improve your overall financial wellbeing. We know tips and tricks to find hidden money, maximize investment returns, and minimize taxes.

Add income. If your cash flow is low, rather than cutting back on your lifestyle and goals, increase your income. See https://www.101money.ca/elevator for tips on how to create multiple streams of income. Other options include negotiating a pay raise or moving to a higher paid position. Note: Many people go back to school to pursue higher education but the results are mixed. Some find higher paid positions while others struggle to find work and are burdened with greater student loan debt.

Add income protection. An illness, injury, or untimely passing can devastate any financial plan. Make sure you’re protected.

There's so much more to learn but I’m trying to keep these posts to less than 3 minutes. If you’d like help with your financial plan, contact me, Tina Michelle Moller, for a complimentary consultation.

The opinions expressed in this blog are my own and do not reflect any other organization. I also claim any errors made as my own. To offer corrections or feedback, please contact me at support@101money.ca. Sincerely, Tina Michelle Moller

Most people create their budget following the advice of many books and financial gurus who’d have you limit your spending based on your income. I do things a little different. Rather than limit your spending, I focus on increasing your income. And seeing we're officially one month into the New Year, now is the perfect time to review your spending habits and create your budget around them.

Action Step 1 - Write down your financial goals

Do you want to travel more? Buy a house? Save for education or retirement? Work less and earn more? Whatever your financial goals are, write them down and figure out how much money each goal will require to achieve. We'll come back to this later.

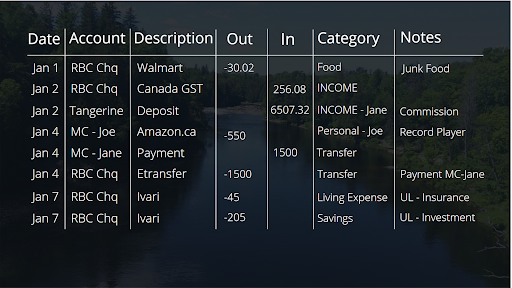

Action Step 2 - Set up a budget tracker using Google Sheets (or other program)

Create columns for incoming information. An example is provided below.

Download each of your open accounts including bank accounts, credit cards, lines of credit, PayPal accounts, etc. for the month (or week).

Organize the information into their respective columns and align the formatting.